Value Traps: The Price of Admission and Shinsei Bank

Value Traps: The Price of Admission and Shinsei Bank

GMO's quarterly letter was out this week and, as usual, gave me plenty to ponder. The main topic being the underperformance of value investing since June, after such a strong run post-election. The naysayers have been circling again, claiming the brief outperformance was a dead cat bounce for an outdated strategy.

The firm's Head of Asset Allocation, Ben Inker, argues the case for a lasting value run persuasively and I highly recommend the whole letter, but the point that jumped out at me most was his discussion of value traps. Answering the criticism that value investing is "hamstrung" by value traps, Inker opens:

"Value traps are a fact of life for value managers. Sometimes an apparently undervalued company turns out to be “cheap for a reason.” Its fundamentals wind up deteriorating faster than expected and with hindsight it becomes clear that the stock wasn’t actually anywhere near as cheap as it originally seemed."

This topic is very dear to me, as most of my holdings have been considered value traps by the market at one point or another (many of them right now). Likely, some of them will indeed turn out that way- I'm just not sure which ones yet.

Fortunately, many of the best investing records are built on 60% success rates, the flipside being that 40% of the managers ideas were losers and due to the assymetric profile of (theoretically) unlimited upside and downside capped at a 100% loss, a portfolio could even do well with a much lower hit rate.

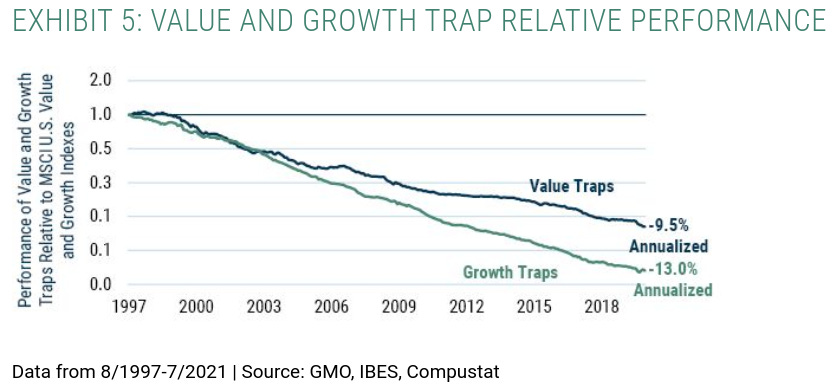

Inker brings up the excellent point that while "value traps" are common in investing lingo, the phrase "growth trap" is strangely absent. I suppose something like "fallen angel" maybe fills the space, but the point is valid. Broken growth stocks are generally much more painful to a portfolio, due to a much wider gap between previous expectations and the new reality, yet because of the roaring growth market of the last decade, value traps are currently more dangerous for a manager's client relationships.

In fact, even given growth's dominance, growth disappointments have lagged their own universe by much more than value traps. Inker defines a "trap" as a business that "both disappoint its revenue expectations and see its revenue expectations come down" in a given year.

Value traps and investor behaviour

In my opinion, value traps are the special sauce that keeps value winning. It is easy to forget that all the historical performance comparisons, showing value beating growth handily over time, also include plenty of value traps. The fact that value shines is likely because of and not in spite of them.

This speaks again to one of the most powerful behavioural constraints in investing- the institutional imperative and career risk (which I touched on recently). Knowing that value investing works over long periods is not enough if you are beholden to short-term flows and liquidity, or just can't take the pain. The fear of buying value traps prevents most from being able to start and stick-with the style.

Additionally, they are typically companies that have left a trail of disappointment in their previous performance. It is a funny place to be, optimistically entering an investment only to encounter jaded and bitter fellow investors, who have much higher cost bases and resent ever having heard of XYZ Corp.

Given the difficulty of picking the bottom, often several new layers of bagholder will be established from this point. It often feels toxic, but this is where excellent returns can happen on very little fundamental improvement.

Being able to sit in these "laughing stock" situations is very uncomfortable and I can only imagine the challenges of presenting the same underperformers to clients each quarter and being asked why you are incinerating their savings. Only being answerable to myself and my family is something I am grateful for and I admire the managers that carry it off.

Again, this strikes at the core of deep value investing- you're not denying some of your companies are dogs or have their warts. But, you think it's more than priced in and maybe something good could happen. The cheaper the valuation, the lower expectations.

My favourite conversation on value traps comes from Pzena Investment Management's principal Rich Pzena, from a 2006 interview with Columbia Business School. When asked how he manages the short-term expectations of his clients, Pzena responds:

"Better to run a business where you promise your clients you’re going to have bad years, which is what we do, we promise them. If they ever ask us, “What about investing in value traps or investing in dead money,” we promise them we’re going to do that too. If I knew which one was going to be value trap in advance I would avoid it! But how do you know in advance?"

I couldn't agree more with this. Value investing without the value traps is akin to a wild night without the hangover- you can dare to dream, but it's not going to happen.

The inverse is also true. It is extremely unlikely an investor will find something at a bargain level with zero risk of deterioration. Waiting for perfect set-ups, that feel nice, with no blood in the water is more likely to encourage paralysis or over-paying. Pzena says it well:

"I think the attempt to avoid value traps is what keeps people from being real value investors, because for something to be real value, you can’t know whether it’s a value trap or not. If it was obvious, if it was labeled that this one was a value trap and that one was not, they wouldn’t sell for the same price."

Nothing to add.

Is it a trap?

As a real-time example, I would nominate Shinsei Bank- a Japanese financial that has been on my watchlist for some time. It has all the hallmarks of a possible value trap- checkered history, sits at multi-year lows, sells for 39% of book and 6x earnings.

Shinsei began life as Long-Term Credit Bank post World War II, to aid financing to Japanese industry. IPOing in 2004, the company needed a bailout by 2011, due to a crushing build up of non-performing loans and retains the government as a large shareholder today, through the Deposit Insurance Corporation of Japan.

Banking has been particularly awful in the Land of the Rising Sun, due to two decades of low rates and challenging demographics, forcing the industry to adapt. Shinsei has done this by developing its growing consumer business, as opposed to many Japanese banks focusing on industrial loans.

Shinsei is adequately capitalised at 11.7% CET1 and has grown book value from 897b Yen in 2018, to 938b Yen today. The company also bought back over 5% of its shares before the pandemic in 2019 and is highly likely to continue it when safe to do so again.

On the negative side, of course, Japan has a well-deserved reputation for cash-hoarding boards, with zero interest in creating equity value. Shinsei hasn't been an exception, with decade-long shareholder JC Flowers (US PE firm) appearing to give up on gaining an attractive return out of Shinsei, selling its stake in 2019 and US manager Dalton Investments failing in its attempt to get founder James Rosenwald elected to the board.

Dalton had also called for an enormous buyback of 200b Yen (around 50% of the register), due to the banks solid capitalisation, but this level seems highly unlikely. With only negligible dividends on offer, it is possible an investment in Shinsei just languishes indefinitely.

Consensus opinion is clear. When suggesting Shinsei as a research target online recently, I recieved this response:

"Shinsei is trash. Crappy franchise, crappy loan book, crappy management, crappy returns. Ever since the LTCB days."

Besides the humour, these things could all be true and Shinsei still be a good investment- it all depends on what you pay. I would argue that Shinsei will do well, based on a return to its pre-pandemic 6% ROEs and slow-burn buyback program.

After all, risking value traps is the price of admission for long-term, deep value outperformance.

Guy

Please don’t take this as financial advice. Do your own due diligence and consult a professional advisor, if unsure about your finances.