Turkcell: You Just Wouldn't Find It This Cheap Anywhere Else

Turkcell: You Just Wouldn't Find It This Cheap Anywhere Else

Ok, maybe besides China. But Turkcell Iletisim Hizmetleri (TKC:NYSE) is a perfect example of a predictable, profitable business with opportunities for future growth, tossed on the scrap heap due to Turkish macro uncertainty and general market indifference to unexciting EM businesses.

Even in traditional telco, which currently has some of the cheapest valuations globally, Turkcell's price could make many of its peers blush- and yet it doubled its revenues (in Lira terms) between 2016-20 and just raised its 2021 guidance to 18% growth. The pandemic gave a boost to additions and connectivity, but Turkey is expected to continue growing mobile subscribers until at least 2025.

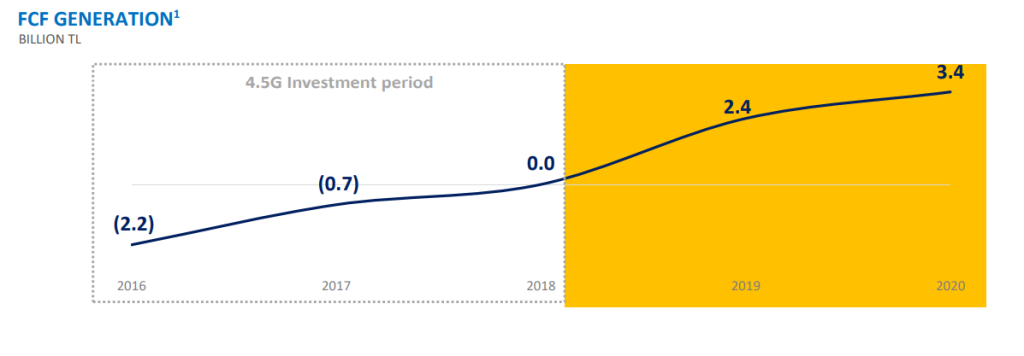

A major positive for Turkcell is its current cash flow positioning, as can be seen from the chart below. The company produced a 10% FCF yield last year, based on earlier heavy network investments rolling-off and starting to bear fruit. It is reasonable to expect that FCF could can be sustained around these levels with further revenue growth likely.

Due to its level of cash confidence, the company will comfortably pay a net dividend yield of 6.2% over 2021. TKC is also the second most liquid Turkish company on the US exchanges, having been only pipped a month ago by the IPO of online marketplace Hepsiburada. There can be unreliable liquidity outside these two, so Turkcell is a worthy name for value investors, who are unwilling/unable to buy on the Borsa Istanbul directly, to investigate.

The Business

Turkcell began Turkey's first mobile service in 1994 and has been a major player ever since, with over 40% of postpaid mobile subscriber share today. The company is led by CEO Murat Erkan, who has been in the role for two years and is seemingly a safe pair of hands.

Like many legacy telcos, TKC has pivoted towards fibre, digital services, IPTV (Internet Protocol TV), leveraging its network and scale to expand these products. There is also a foreign presence through subsidiaries in the Ukraine, Belarus and Northern Cyprus, currently bringing in around 8% of revenue.

Turkcell's major competitors include Turk Telekom and Vodafone Turkey, both of which trail on mobile subscribers. However, TT is much more advanced in its fibre businesses, with 8.1m fibre customers (although 5.6m of these are less impressive Fibre To The Cabinet connections) dwarfing Turkcell's 1.8m. Similarly, TT has 3m IPTV subscribers, ahead of TKC's 1m. These are an area of concern, as TKC has major fibre capex ahead of it to match its rival, although this part of the business can hopefully grow strongly off its small base.

Throughout 2020, the company added 1.6m mobile users and saw mobile ARPU jump 15%. Its Superbox product gained 591k subscribers, which allows supposedly fibre-like speeds to households over its mobile network. Whether this product is a threat to its own FTTH growth is a possibility (while this is cheaper to provide, barriers to entry are much lower), but it seems a strong way to leverage its mobile muscle.

The advantages of incumbency can be plainly seen through the uptake of Turkcell's fintech payment platform Paycell, which as of June 30, had reached 5.5m active users and seems likely to grow given exposure to the company's 34m mobile subscriber base.

As a further point of interest, Turkcell has a 23% stake in the TOGG project which aims to produce Turkey's first domestic EV, using Lithium from Turkish mines. Capital wise, it appears to be fairly inconsequential to the company, but may have some marketing/image benefits. First production has been targeted for Q4 2022... so look out Tesla!

Financing is extremely conservative at the company with net debt/EBITDA a modest .7x. The company could surely handle significantly more with its cash-flow profile, but guaranteed survival and flexibility have value too. A large debt-funded buyback would be extremely value accretive, but seems unlikely.

On the whole, TKC is a just a steady player in a stodgy industry doing many things right, but being ignored for its efforts. In Lira-terms, the market cap is where it was in early 2018, despite the steady growth in revenues and EBITDA recorded since. Of course in USD-terms, the stock is a disaster, halving over the same time frame.

The percieved macro red flag

Of course, it is hard to deny that Turkcell is cheap, the red flag for most investors is its Turkish domicile: more specifically, Erdogan's presidency and the interminable depreciation of the currency.

Following the 2016 coup attempt, Erdogan pushed through an aggressive 2017 referendum which estabished him as possible/likely leader until 2029, by elevating the presidency and eliminating the prime ministership. Since this time, Erdogan's autocratic leadership and erratic monetary policy have been largely credited with the capital flight from the country.

His continual firing of Central Bank chiefs hasn't helped, with three being axed in two years, most recently Naci Agbal in March, who had been seen as a stabilising force by markets to that point.

The Lira has lost nearly 90% of its value against the USD since 2008. Truly ugly, but this may not be the widow-maker trade that it seems. Firstly, the EM bubble that peaked around a decade ago greatly overstated the true value of the Lira, while understating the USD in it period in the doghouse, post-GFC.

Secondly, on comparitive measures that adjust for relative wealth, the Lira is now showing as deeply undervalued. This is true of both the traditional Purchasing Power Parity (PPP) and the famed Big Mac Index, which currently shows the TRL undervalued by 59%.

This is also patently obvious when observing Istanbul apartment prices vs peers. At $1.3k/m2, the city is priced similarly to Dhaka, Kathmandu, Addis Ababa and Quito, all of which have much lower GDP's per capita, living standards and lack Istanbul's pizzazz as a cosmopolitan giant.

Thirdly, Turkey's Current Account was plunged back into deficit at the onset of the pandemic and has been recovering since. As seen below, Turkey reached a deficit of $5.9b in March 2020, while June 2021 has seen a drastic recovery to $1.1b. This speaks to the FX drought Turkey has seen since the pandemic began, primarily through the halt of international tourism and continued reliance on imports over this time.

It seems reasonable that this recovery can continue if the CA really is approaching a sustainable balance. The cheap currency should even play a large part in enticing back tourism and investment.

Further, as a largely domestic services company, Turkcell has no reliance on imported goods, meaning its operations will be unaffected by currency pressure. The company also holds 87% of its cash in USD and has hedged 41% of its debt in TRL, so should theoretically lose much less value than the currency in the event of further devaluation.

Valuation

Without giving an exact fair value target, I will explain why I believe TKC is unlikely to hurt the long-term investor and and has a lot of pathways to surprise on the upside. The business trades for an EV/EBITDA of 3.1x this year's expected 14.3b TL. Given competitive pressures, I think it is wise to base a fair value estimate off a no-growth assumption, even though it will probably prove conservative.

In my opinion, fair value for Turkcell lies at 7x EBITDA, which seems unrealistic today, but would be very achievable over a cycle in an environment where Turkey is no longer considered a basket-case. After all, the company traded at 9.6x back in 2015 and 6.8x as recently as 2017. This would give an enterprise value of 94b TL and market value of 84b TL after subtracting current net debt. Adding back 11b TL in dividends lands at an expected 2025 value of 95b TL.

As an additional safeguard, I will bake 15% pa currency depreciation into the expected return, even though I consider this unlikely and that Turkcell would outperform this scenario, as argued above. Our 95b TL depreciated at 15% over five years erodes to 42b TL (current market cap 35b TL)- a miserly 3.8% pa, but non-fatal.

I realise this isn't a conventional way to value an asset, but the goal is to show just how negative the next five years would have to be to lose money. Any positive surprises would be a bonus, remembering we are factoring no growth in revenue, cash flows or dividends, no debt pay-down, a reasonabe multiple and highly punitive ongoing currency devaluation. Conversely, a world where the Lira could stabilise against the USD would result in around a 3x or 25% IRR over the five years. I think the true result will fall somewhere in between.

I am currently analysing several Turkish companies and definitely don't consider myself an expert, so all pushback is welcome. Thanks for reading.

Guy

Please don’t take this as financial advice. Do your own due diligence and consult a professional advisor, if unsure about your finances.