Ping An: Growing Like a Weed, Priced to Liquidate

Ping An: Growing Like a Weed, Priced to Liquidate

As I argued a fortnight ago in my post covering Melco International, CNOOC and Greatview Aseptic, I believe there are higher probability ways of taking advantage of the ongoing Chinese CCP-inspired bear market than Alibaba and Tencent. In that piece, I presented three stodgy companies growing much slower than the tech favourites, but likely to do better due to their extremely cheap valuations, in my view.

Today I want to single out a business that has been growing at a phenomenal rate and is more of an improving Chinese living-standard beneficiary than almost any other- Ping An Insurance. The world's second largest insurer (after Berkshire) at a $145b market cap, which has grown book value at an impressive 23% pa since going public, in 2004.

The conglomerate has declined 40% this year after being caught up in the China Fortune Land default, booking an impairment of $2b on its investment which dragged down H1 net profit down by 15% YoY. Ping An was also rocked last week by a report that the Chinese regulators are probing its property exposure and have ordered a halt to its sale of property-realted alternative investments as part of a wider crackdown on the over-heating Chinese real estate market.

In my opinion these fears are over-blown. Firstly, Ping An's total property portfolio is $29b, so even assuming a catastrophic 50% write-down across the board would only impair shareholder's equity by 12%. Not pleasant, but very survivable with the extremely profitable core division intact.

Secondly, the existing impairments have been non-cash, with operating profitability and cash generation as strong as ever through the first half. At today's price, you could view Ping An as buying only the fast-growing Life division at 10x operating profit and 1.08x Embedded Value (EV or the present value of written policies + current NAV- a P/EV of 1 would assume an insurer never writes profitable business again), with the rest thrown in for free.

Thirdly, China's real estate market is still functioning, even if it looks bubble like to an outsider. Lowering property exposure to appease CCP dictate now could be considered "panicking early", with now a reasonable time to be selling down holdings. Admittedly, the credit implosion of China Evergrande has reverberated through the market, but the Chinese insurers are believed to have been lowering exposure throughout the year.

The business

Ping An was founded in Shenzen in 1988 and its name is translated as "safe and well". The financial powerhouse's network spans insurance, healthcare, technology, wealth management, banking and auto. Its most material division, by some margin, is its life and healthcare operation Ping An Life, which accounts for around 2/3 of operating profit and earns an impressive 35% ROE.

This division has earned Ping An the status as the only Chinese insurer designated as "systemically important". While extra government attention is surely an overall negative, I would argue that the CCP is currently significantly de-risking the business, not a bad thing in a market with potential credit risks, despite the company already generously meeting its capital requirements. I see the company as so cheap that there is room to clear out any potential skeletons in the closet, in the event of further credit concerns or volatility.

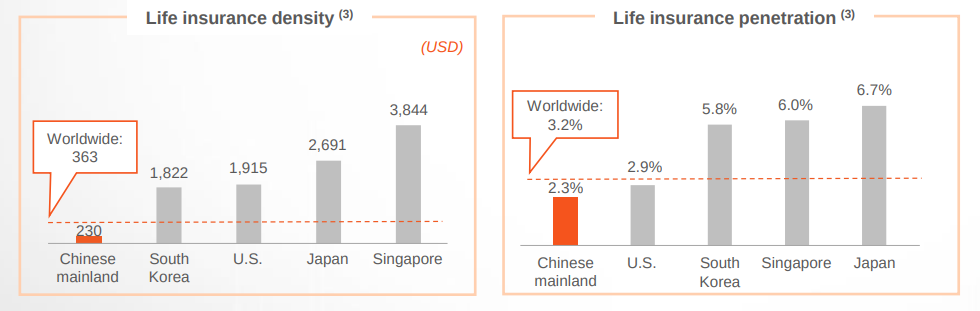

Property and casualty insurance is another strong division, producing a combined ratio of 95.9% in 2021 H1. It is these two insurances businesses that make Ping An such a major benificiary of China's rising living standards. As the middle class continues to grow, the gap will close between current low insurance penetration rates and those of Asian neighbours.

The charts below highlights early China is in life insurance adoption and the company's significant potential tailwind:

In banking, Ping An Bank was formed through a strategic position in Shenzen Development Bank, which became part of the group. Pre-covid, it generally earned ROEs of 10-12% and managed 9.6% in a challenging 2020. The bank has grown steadily and produced $4.5b in net profit last year. In my opinion, this performance deserves a price of book value or 10x earnings- roughly 1/3 of the parent's current market cap.

On the technology front, I have seen plenty of write ups (and done a few myself) of EM companies mentioning a small tech division that may or may not become material to the group. Whereas, Ping An's fintech and healthtech portfolio is already impressive. For example, the company currently has 34,920 (not a typo) patents under review.

The size of its customer platform has also allowed the development of several highly succesful early stage companies, most notably Nasdaq-listed Lufax Holdings (Ping An's stake worth and HK-listed Ping An Good Doctor. Lufax is an online wealth management and peer-to-peer platform with around 15m investors and borrowers, which grew revenues and users 16-17% YoY, while Good Doctor (formerly Ping An Healthcare and Technology) produces health services software allowing online medical consultations, referrals and health management, with 400m registered users (29% of the population) and grew revenues 39% YoY. These two stakes were worth $10b at June 30, however both are down since, in sympathy with the parent.

Another significant use of technology has been Ping An's use of AI to streamline Ping An Life. For H1, the company was been able to reduce its number of insurance agents by 15% YoY, while increasing FYP (first year premium) per agent by 24%. AI has made recruitment, applications, health checks, staff training and ongoing management continuously more efficient.

The CCP issue

Much has been made of the recent crackdown by the ruling Communist Party's recent efforts to stamp its authority over enterprise. There is a non-trivial risk that any foreign investment in the country is left worthless, given that political tensions are inherently unpredictable and the CCP, perhaps even less so.

To many, this has ruled China "univestable", but I don't see the issue as black or white. While I think it would be insane to have +50% of a portfolio invested there (especially given other attractive emerging market alternatives), there is a price point where the regulatory risk can be compensated for.

Equally, as has been stated elsewhere, an asset seizure would be highly damaging to China's interests, with the cut-off of foreign capital that would ensue. I don't see this as a very high probability. Other possibilites include continual grift placed upon the company, such as Tencent's recent forced "contribution" to the sustainable social values fund, which I referenced in my earlier article.

Indeed Ping An's success may be cause it problems down the road. While the government has a strong interest in Ping An's solvency and strength, it has shown very little regard for monopolistic profits in other industries. This is a much more likely situation, in my view, where the company is unable to flourish to the same level as in a free market economy, through "contributions", overly high capital requirements and possible pricing caps down the road.

Finally, I should mention the persistent and highly intelligent vocal China bears, who have consistently called for an implosion of the Middle Kingdom's economy for the last 5 years or so. They count some of the wisest minds in finance in their ranks, including Jim Chanos, Kyle Bass and Crescat Capital and I am nervous to dismiss their claims out of hand. There is no doubt China has used credit extremely liberally to finance its expansion, but I have no idea whether it will ever matter.

In my view the solution to all of the above is to manage China exposure to a level that makes sense for your own portfolio. A starter position is normally 6% for me, so I have set a limit at 12% of my portfolio at position inception. Not putting too many eggs in any one basket is the best way to limit CCP, VIE, macro, credit, geo-politicial risks at the end of the day.

Valuation

Ping An is cheap, there's no getting around it. The business currently sells for 6.5x earnings with an extremely well-covered 4.4% dividend yield. These are the sorts of numbers I am used to seeing, while holding my nose looking through deep value companies. That they come with an industry dominant business, which achieved a 19.5% ROE last year in tough conditions, has grown EPS 23.4% pa since IPO and announced a buyback with its interim earnings, with more likely to come is... quite attractive.

I believe the demographic and economic tailwinds behind Ping An are so great that the friction of CCP interference will be more than made up for. But for those who are skeptical and blame a China discount, consider that competitor China Life currently sells for 17x 2020 earnings with an ROE of 12%. Even taking 2019's stronger results, China Life is both substanitally more expensive and less profitable than Ping An on 15x and 16%.

There are numerous back of the envelope ways to value Ping An. I am merely trying to assertain that a wide margin of safety exists in a base case future and let any positive surprises take care of themselves.

For example, Ping An is selling for 70% of the current Embedded Value of the whole group (not just Life, as mentioned above), implying that it is not only being wound down, but the pieces only recouping 70c on the dollar. Given that group EV has doubled in the last five years, and is showing no signs of slowing, this is just fanciful.

Alternatively, extrapolating this out at 15% growth (lower than current run rate) on 2020 operating earnings for five years would give an expected 2025 operating profit of 281bRMB. Applying a fair value multiple matching China Life's 15x 2019 earnings, I estimate an expected 2025 market capitalisation of 4.2trRMB or 4.5x today's price. I believe all of these assumptions are defensible and fairly conservative, with a growing dividend on top.

In my opinion, Ping An is a fantastic opportunity to take advantage of the current China panic-selling.

All feedback welcome and thanks for reading,

Guy

As always, this isn’t investment advice. Please do your own due diligence and seek professional advice if you’re unsure about your finances.