Millicom: Special Sit Dynamics Throwing Up A Bargain

I try to follow the Buffett, punch-card approach to portfolio management and, accordingly, have barely transacted in the last year. But a set-up is emerging that may be one of the most attractive I have seen in several years.

Millicom’s (NYSE:TIGO) share price has been under severe pressure since late last year, in part due to the strengthening USD and weakness in the telco sector, but laregely due to uncertainty around a now-announced Rights Offering to fund the buyout of their Guatemalan JV partners, for $2.2b.

The terms of the issue are quite similar to the rights offering Liberty Latin America (LILAK) undertook 18 months ago, and I believe there is a good chance they will follow the same playbook. Essentially, in the days before trading in subscription rights closes, there will be an arbitrage available that may see TIGO common stock fall surprisingly close to the subscription price of $10.61/share. The tail will wag the dog.

I personally have no interest in the arb, but at those prices, I believe the common stock would be an astonishing bargain.

A brief background

Millicom is a Central and South American-focused telco, dominant in most of its markets, with the largest being Guatemala, Colombia, Panama and Paraguay. Like LILAK, the company has western management with an eye on shareholder value, with headquarters in Luxembourg and listings in New York and Stockholm. The company has been aggressively rolling-out cable in geographies with penetration rates a fraction of developed peers. The runway is genuine and substantial.

The company has been very deliberately shaping its focus in recent years, having completely exited its African operations (7 countries since 2015) and locked in leading positions in its preferred markets, organically and through $4.7b of acquisitions since 2018. I believe, long-term, the struggles of Latam economies will have been a net-positive, by allowing them to acquire very cheaply and grow their business with little competition.

The most recent of these acquistions is the buy-out of the minority (45%) stake in Tigo Guatemala, priced at a very reasonable 6.2x EV/EBITDA and 8.2x Operating Cash Flow. While the market has sold-off at the prospect of dilution, these assets are among Millicom’s most attractive, will bring in substantial Free Cash Flow immediately and are obviously highly synergistic, given the company is already managing them.

The $717m raise will create 70m new shares, increasing the count by 70% to 171m, and the capital structure will remain well-levered at around 3.1x EBITDA (incl. leases). Millicom closed the Guatemala deal the day after it was announced, using bridging finance, so the capital raise will do nothing to the enterprise value and merely reinforce the balance sheet.

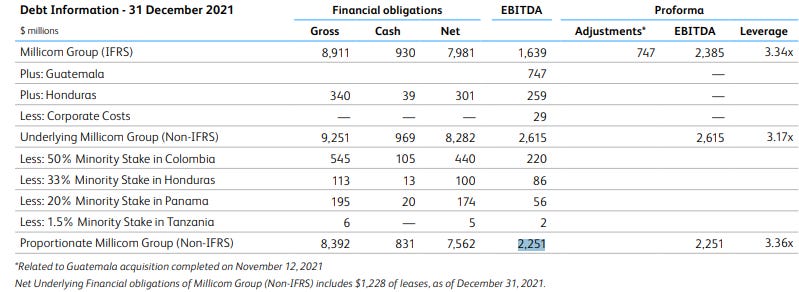

At the current price of $17.10/share, TIGO looks like a steal at an EV/EBITDA of 3.76x. Using a $1.74b market cap, $6.71b Mar 31 net debt (ex. leases) and the company’s 2021 Proforma EBITDA of $2.25b. As shown below, this is higher than the IFRS number, but is more accurate for valuation purposes, as it adjusts for the Guatemala debt’s immediate addition to the balance sheet, while the operations only contributed to income for the last 7 weeks of the year.

The Rights Offering dynamics

I can give no guarantee that the TIGO capital raise will play out the same way as LILAK’s, but the similarities are striking (TIGO press release here).

In September 2020, LILAK raised $350m to fund it purchase of Telefonica’s Costa Rican assets. Again, it was a sensible acquisition at a good price (which I wrote about at the time here). I finished that piece by saying:

“I will participate in the raising in full and look to add further shares on weakness as I believe the combined entity will be more stable, is successfully building scale in growth markets and very cheap in relation to its cash flow generation potential.”

Little did I realise just how much “weakness” there would be. After trading at $10 before the offering, LILAK stock swooned as low as $7.50 in the days before the subscription rights expired, compared to the subscription price of $7.14.

The reason being that both Issues are structured with all shareholders (as of May 23 for TIGO) receiving subscription rights giving the option to buy at a given price in the final placement ($10.61 for TIGO). These rights are then tradeable, to compensate those who don’t want to participate with the option to sell them.

But in reality, the tradeable window for LILAK rights was so short (it will be May 27-June 8 for TIGO) that many were confused and wary of getting caught with rights that were worthless if unexercised. This caused a downward spiral as the rights plummeted downward over the last few days, eventually changing hands as low as 30c each.

While this was happening, an arbitrage was available to short the common and buy cheap rights to be exercised. This caused the common to fall too, until a couple of days before trading finished (it wasn’t the final day), the market seemed to realise that jerking a $2b market cap, with multi-decade duration, around because of 30c rights (that would expire in 48 hours) was a bit stupid.

At the time, I agonised over adding heavily before the entitlement period to get more rights, how to load up for the over-subscription privilege and then whether to buy more rights on market. In reality, the available over-subscription allocation proved minimal and the buying the rights simply added a layer of complication by funding and going through the conversion.

But in the end, the common simply got so low that I was able to load up at an outstanding price, just like any outsider could have. LILAK traded at $15/share less than a year later, although it has been dragged back down in the recent malaise.

As stated earlier, it remains to be seen whether TIGO’s Issue follows a similar path, but the share price has already reacted violently to the announcement of terms. The capital raise has been known to be coming since November, so it really shouldn’t have justified last week’s swan dive.

One large difference is the TIGO terms are at a larger discount to its common stock price and this may cap how far the market would let things fall before coming to its senses. As a market tragic, it will be fascinating to watch it play out.

Strategy going forward

There are quite a number of telcos in emerging markets that can be bought at under 4x EV/EBITDA. I own a few of them, such as Telefonica Brasil and KT Corp, but you are generally buying on the outright cheapness of the business and hoping they will muddle along, pay down some debt and maybe even do a few buybacks along the way.

However, it is astoundingly rare to see such a low price for a business with western management casting a long-term eye towards the Malone-style, geared buyback model. The current CEO, Maurico Ramos, came to Millicom from the role of Liberty Global’s President of Latin America (before LILAK existed), so he is well schooled in the dark arts of financial engineering.

For example, the company owns over 10k telecom towers, that it has said it will sell and lease back within the next 12-18 months- seizing the attractive multiples being paid for infrastructure assets with rates so low. These could be a significant source of return, with Telefonica Brasil’s recent sale of 1655 towers for $214m implying $1.3b of hidden value ($130k/tower), or over half the market cap, even post raise.

The company also has a fintech division, Tigo Money, that is growing fast and had over 5m users and $50m in revenue in 2021. To be honest, I have little idea how to value this, but am happy to consider it a free option that could be quite valuable down the track.

Most importantly, capital allocation priorities will be focused on deleveraging and buybacks. Malone vehicles very rarely pay dividends, due to their hatred of taxes, and TIGO follows this spirit. The company has committed to reduce leverage to 2.5x EBITDA by 2025, indicating either $1.4b in debt paydown, earning an extra $3.1b in EBITDA or likely a blend of both. Buybacks are set to resume in 2023.

Regular readers will be bored of me saying it, but this is the classic Dan Rasmussen framework of a small, cheap company paying down debt and creating equity value, while strengthening the balance sheet. Even a modest, upward re-rating of TIGO’s EV/EBITDA would give impressive levered returns, but I think fair value is ultimately around 7x in a market that is prepared to reward stable, cash-generative, non-US businesses again.

So time will tell, but I believe Millicom is a great buy here and may become the sort of opportunity you only see every few years if it falls lower over the course of the issue. I don’t know TIGO as well as I would like yet and am trying to rapidly get up to speed, so please reach out if I’ve missed or overlooked something.

I own shares in LILAK, Telefonica Brasil, KT Corp and I hope to acquire shares in TIGO over the next fortnight.

Guy

I hope it is abundantly clear to anyone reading this that I’m not a financial advisor and not giving anyone financial advice. I am writing my own thoughts and the rationale behind my decisions in the hope they are entertaining to others and open up a dialogue from which I can learn something. There have been recent law changes in Australia drastically curbing those who are allowed to discuss investing in the public domain and while this currently doesn’t effect me, it is likely to at some point and may have future implications for this blog. In the meantime, please do your own due diligence and seek the assistance of a financial professional when managing your investments. This is certainly not a recommendation to buy TIGO shares, or any others mentioned in this article.

Thanks so much for the write-up. Does the thesis remain intact after the big drop of the last 6 months?

Any idea how much cashflow they have to give up for "rent" after selling the towers?