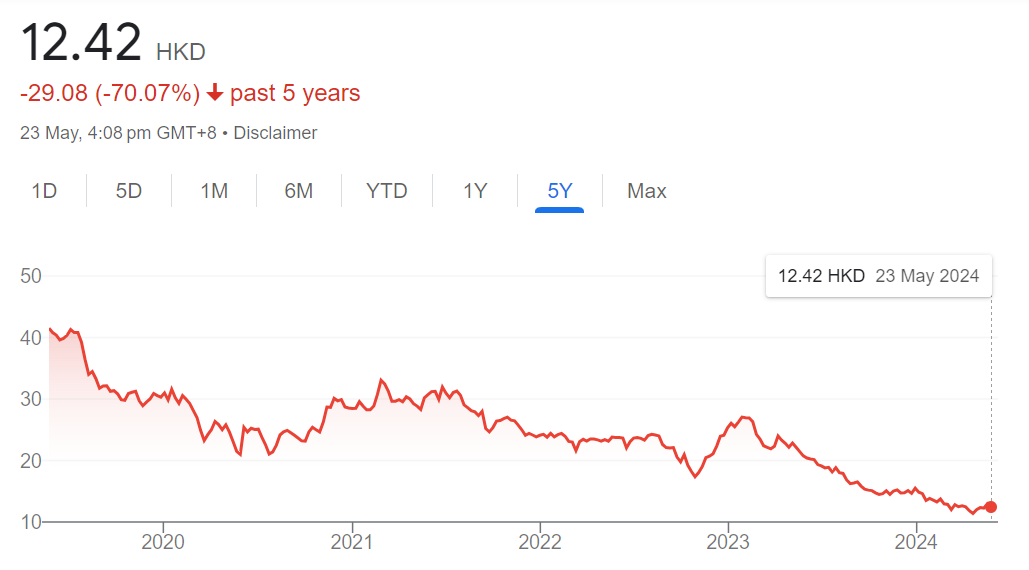

Hysan Development: Maximum pessimism

Earlier this week I presented Mandarin Oriental as a low risk, special situation way to buy Hong Kong real estate. In contrast, today I will summarise my view of Hysan Development, a HK-listed developer with no special situation element at all. Despite a high-quality portfolio centred around one of the city’s best retail districts (Causeway Bay), Hysan is simply table-pounding cheap. In my view, it has been caught out as a relative small cap in a sector where even the largest bluechips are currently uninvestable.

Without wanting to flatter myself (I bought the stock yesterday), I believe this is the sort of situation John Templeton would have swung at. This is what maximum pessimism looks like.

There simply isn’t anything wrong with the company. An investor just has to embrace the uncertainty of the Hong Kong property market and I would argue the margin of safety to do so is very adequate.

The Company

While unfamiliar to most investors, last year Hysan celebrated 100 years since the purchase of its flagship property Lee Gardens by its founder Hysan Lee. Fascinatingly, Lee himself was also involved in the narcotics trade and was eventually assassinated, supposedly due to a rift with Macau rivals. Headlines at the time referred to him as Hong Kong’s “Opium Prince”.

His family has stewarded the business ever since, with their holding company Lee Hysan Co owning 42% of Hysan Development today and four members of the Lee family featuring on the board, including the chairwoman Irene Lee (granddaughter of Hysan).

The company develops and leases prime commercial real estate, predominantly situated within the Causeway Bay district. While it has a roughly equal exposure to office and retail, retailing is its strongest suit with Louis Vuitton, Chanel, Dior and Hermes expanding their presence in Lee Gardens recently.

Hysan’s Causeway portfolio can be thought of as an interconnected commercial network and new walkways under construction will link Lee Gardens and enhance their desirability. The new jewel in the crown will be the Caroline Hill Road project due for completion in H2 2026, adjacent to Lee Garden Three and Six.

The site was purchased by Hysan in 2021 in a 60:40 JV with Chinachem Group, via an auction by the HK government which attracted robust bidding. The share price since shows the deep scepticism the market feels for the HK$19.8b ($2.5b) price tag and the risk of an empire-building mentality.

Before the deal, Hysan was a net cash company and today it carries HK$21.7b net debt and a net debt/equity ratio of 27.2%. While I acknowledge this is a decent chunk given the uncertainty and pressure surrounding the market, it should prove manageable under even the most negative scenarios. If only your typical Australian developer showed similar restraint.

The Caroline Hill site is such a seamless fit for Hysan it is easy to imagine why they likely overpaid to acquire it. As a silver lining, the company secured advantageously priced green financing and cut the final dividend by 25% earlier this year, showing they will measure the leverage prudently. When a family’s pride and prestige is tied to a century of building a company (especially in Asia), they are very unlikely to moonshot it away. I expect the company will continue to be run conservatively with a nod to the next 100 years.

Regardless, one of the beauties of value investing is picking up assets on the cheap after others have paid for past sins.

Strategy under uncertainty

Irene Lee appears a competent operator and excellently connected. She is a trained barrister and on top of her leadership at Hysan, chairs the board of Hang Seng Bank and is a director at Alibaba.

Last year, when asked whether she had more confidence in the company’s retail or office markets, after first admitting more optimism about retail, Lee responded:

“We actually see office and retail as fairly integrated or combined. So if the office floors are slowing down, I will actually carve out some and make them semi-retail. So I’m very lucky that we can be (flexible) and we see it as an integrated portfolio.”

Inversion at work

A major reasons for such deep discounts at leveraged HK developers is the uncertainty about future property valuations. There is a sense that China is going through a “reckoning” and there is no floor on where values could end up. When investors look at a balance sheet, they fear the investment property item collapsing and the debt remaining ever constant.

Putting aside that Hong Kong is an already established global financial centre, property there is geographically constrained, tourism is still returning to normal post-Covid with signs this is advancing well and that the island bears little resemblance to Chinese mainland tier two and three cities with questionable demand- let’s consider the company’s valuation and what it would actually take to lose money.

Below are the asset side of Hysan’s balance sheet and investment properties broken out by category:

If we:

Purge the balance sheet of all assets except for investment properties, cash and deposits (no value for the group’s stake in Grand Gateway 66 in Shanghai and write off JV loans).

Write down office, residential and property under development (Caroline Hill JV) by 50% and retail by 33%.

Subtract total liabilities (HK$35b)

We reach a liquidation value of around HK$22b- still 76% above today’s market cap of HK$12.5b. Further, we are paid an 8.9% dividend to wait.

It’s in the eye of the beholder whether this is a harsh enough worst case scenario for the company, but one thing I’m sure of is the day the market believes Hong Kong property has bottomed, Hysan will be trading substantially higher than 19% of book.

I’ve got to give a nod to phil_hk and Michael Fritzell for mentioning the company and bringing it to my attention. They have boots on the ground in Asia and I’m very grateful.

Thanks for reading,

Guy

I own shares in Hysan Development.

As always, this isn’t investment advice. Please do your own due diligence and seek professional advice if you’re unsure about your finances.

Thanks for highlighting Hysan, and Mandarin Oriental in an earlier post. Of the two, Hysan would certainly appeal to me more, not least because its share price is trading at nearly a 20 year low, and the substantial discount to its NAV should narrow when outlook turns rosier.

MO, by virtue of its Jardine's parentage, is a much "sleepier" company and unlike Hysan, do not have a history of rewarding its shareholders with a decent DPS. Yes, the discount to its RNAV is there but does that have a realistic chance of being realised? I think not. Even when there was a massive offer for the excelsior hotel site a few years ago, which far exceeded MO's entire market cap at that time, Jardine refused to sell and determined that they were more keen on its own empire building. I would not be the first to take issue with corp governance issue there.

Apart from Hysan, perhaps you could take a look at Tai Cheung too. The latter is a smaller company, trades at similar sized discount, pays a decent dividend as well, but one thing that sets it apart is that it has no debt and in fact its net cash position roughly equates to 2/3 of its current mkt cap. Michael Fritzell has written up a good write up on the company here https://www.asiancenturystocks.com/p/tai-cheung-88-hk. Of the three, i favour TC most and MO least.

I unfortunately had the unpleasant experience of owning Hysan slightly longer, with a high teens entry price. I take a much less optimistic view on management. Hysan has also developed a habit of poor capital allocation, mostly funded by debt and pref equity.

The Caroline Hill Road project was as close as possible to the Lee family igniting money on fire. They funded that project with 100% debt, which will need to be refinanced in coming years. By my rough estimate, unleveraged yield on cost will be sub 4%, well below Hysan’s current cost of debt.

Hysan’s foray into the healthcare business has also been a disaster, from what I can gather that business is generating negative margins. Hysan’s speculative Mainland office purchased from CKH has had close to zero occupancy for years. Oops. Hysan’s residential apartments, Bamboo Grove has also had laughably low occupancy, despite its prime location.

Hysan has also been caught off guard because some of its pref shares are converting from fixed to floating, which wil likely cause another dividend cut. Oops. They alluded to this during the last semi-annual webcast. As far as I can gather, management does not show much self awareness and analysts do not hold them to account.

My only reason for still owning the stock is hope that the Lee Family might be forced into selling some assets, and change its behavior, as negative leverage of higher interest rates has made prior mistakes too obvious to ignore. I agree that there is value here, but is it trapped value or a value trap? I am close to 50/50.