H1 2021 Portfolio Review

H1 2021 Portfolio Review

For the six months to June 30, I gained 21% in AUD, when compared to the MSCI ACWI IMI, which gained 13.5%. On a constant currency (USD) basis, I was up 24%, due to a modest decline in the Aussie Dollar over the period.

More importantly, since I began formally tracking my portfolio in Aug 2018, I have gained a cumulative 31%, modestly underperforming the MSCI which has returned 36% (both in AUD).

The biggest contributors for the half were longer-term holdings Gazprom, Cameco and Micro Focus, as well as new-comers Petrobras and Babcock International, while the biggest detractors included ABS CBN, Barrick Gold and Saipem. It needs to be noted, however, that Micro Focus dissapointed on earnings in early July and has since fallen around a third. Much of the portfolio has also had a tough few weeks, with global value apparently on the nose again- but that will be a problem for the yearly review!

Antero Resources also deserves a special mention for nearly tripling over the first half. The stock is now hearteningly close to breaking even on my excruciatingly timed buy at $19 in late 2018. If you have ever heard the analogy made that someone who held Amazon from the 90s till today would have had to hold through a 95% drawdown in the Tech Wreck, consider that Antero finished the half at $15, having taken the trip via 77c!

The portfolio currently has 15 positions, including four new investments added over the period- namely Petrobras, Telefonica Brasil, Babcock International and Saipem. All are typical of where I continue to see the best opportunities- global deep value.

Mobile Teleysytems, Greenlight Re and Landsec were sold, despite what I still consider to be appealing prospects. Unfortunately, something had to give to accomodate the outstanding potential I saw in my new positions and maintaining a little dry powder, given the continuing nosebleed valuations and froth in the headline markets.

Jardine Strategic also left the portfolio after it was bought out by its parent Jardine Matheson at a price that was a nice short-term bump, but still well below where readers will know I saw long-term fair value (see here). This is the sort of circumstance that can frustrate the life of a minority shareholder, but I have recycled the funds and will just have to get on with it.

The index remains an afterthought and I continue to only calculate my relative return on a half-yearly basis. I am now only slightly down on its performance since my inception and am quite confident that I will outpace it in coming years when I look at the coiled springs I see in my portfolio, compared to the bloated, frothy and growth dominated S&P 500 and MSCI World. If I had known how badly deep value would underperform for the next three years in 2018, I would have been happy to be this close and am delighted for the prospects going forward.

My cash position came down slightly over the half, from 16 to 12%, due to portfolio appreciation and activity. This continues to be my largest challenge- balancing attractive investments with the ability to deploy on further weakness. What seems cheap today may be run of the mill in a future opportunity set and I want to have a little flexibilty to react.

Some may call this market timing, but with indexes near record highs, I call it common sense. Despite the Buffett quotes to the contrary, Warren seems to find himself on a pile of cash near the end of roaring bull markets and months like July so far tend to support this view.

Of course being 88% invested also speaks to the bargains I believe exist today and these continue to be clustered around my three pillars of EM value, the UK and energy (which I detailed here). I consider these markets as fishing where the fish are and expect they will produce attractive returns for many years as they return to favour.

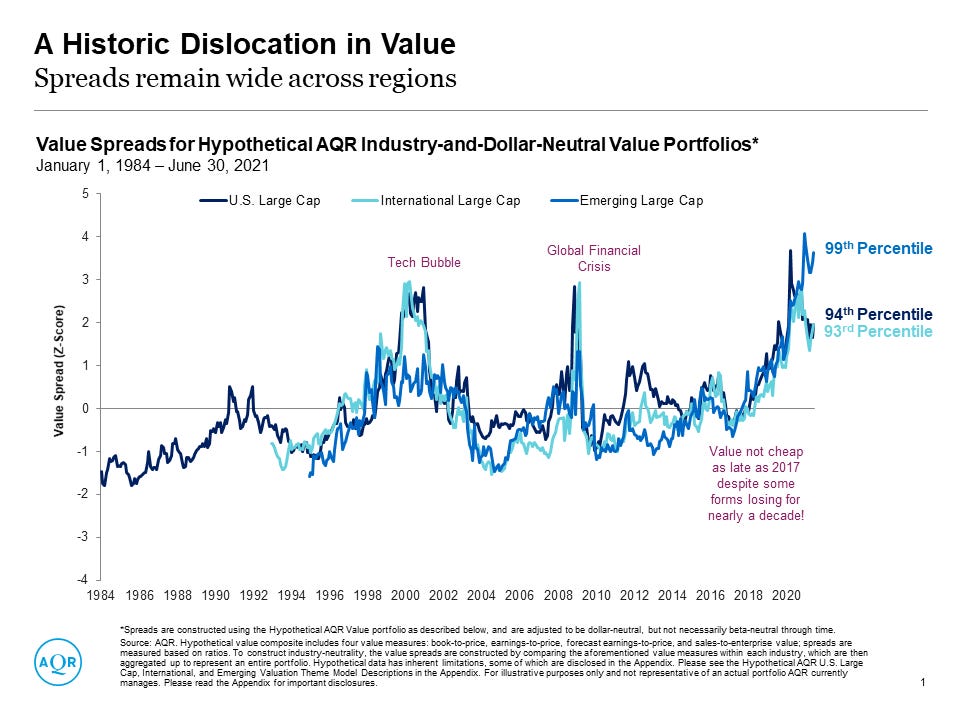

The chart below from AQR is highly illustrative of how historically wide the spread still is between growth and boring/uninspiring value companies.

My energy holdings continue to make up around a third of the portfolio including exposure to gold, oil, nat gas and uranium.

Top Positions

Aimia (12%)-

Aimia continued to chug along in H1, reaching a deal to convert it's stake in Air Asia's loyalty program Big Life into a direct holding in Air Asia. The company is using its cash (135m CAD on the balance sheet) to invest in undervalued global businesses such as Clear Media, JC Decaux and Newmark Group. Its stake in the Mexican airline loyalty program PLM remains it most significant asset.

Management has been proactive continuing last year's significant buybacks and I am delighted to have them as stewards of my largest holding. I see fair value at around $6/share (current price $3.61 USD) and most significantly, I view Aimia as a growing discounted pie that I hope to hold for some years yet.

Liberty Latin America (9%)-

One of my two Latin American telcos, Lilak has retained the resilience it showed throughout the worst of the pandemic into 2021, continuing to grow its subscriber base and tucking its newly acquired AT&T assets into the fold. I remain bemused why the share price was brutalised the way it was last year, given its competitive advantages, management quality and revenue strength.

My large purchases around the capital raise last September have borne fruit with the price gaining 80% since, yet despite this, it remains modestly valued at 6.5x EV/OIBIDA. The company is well on the John Malone-model path of growing fast using leverage, then cannibalising itself through repurchases and will be a large winner over the next decade in my opinion.

Micro Focus (9%)

I'm a sucker for a turnaround and Micro Focus continues to be a high conviction position. It remains very cheap due to its UK domicile, large debt and past sins (the shocking acquisition of HPE Software in 2018). The company today is something of a cash cow, however, with management laser focused on disciplined capital allocation through debt paydown and the reinstatement of a small dividend.

Revenues are admittedly still declining, although at a slower rate, and licencing was strong in H1 which should lead to stronger maintenance performance in future periods. As mentioned above, revenues and cash conversion disappointed in early July sending the price down significantly. I will continue to monitor the position closely and think the company remains an ideal takeover candidate. Here is my recent write-up on Micro Focus for those interested.

ABS CBN (8%)

I remain very bullish on ABS CBN despite its ongoing stoush with Filipino president Rodrigo Duterte. The media conglomerate remains extremely undervalued relative to its services/subscriber business, trading under a third of my fair value, with even more significant upside to be realised if it can broker a return of its broadcasting franchise.

A media broadcaster without the right to broadcast its programming seems like a ridiculous situation (which it is), but it is also why the security is one of the most appealing I have found globally. Please find my detailed write-up of ABS CBN here.

Babcock International (7%)

Another UK turnaround (sigh)! I purchased Babcock at a 15 year low in January after the company again downgraded earnings guidance and Barclays published a report anticipating a capital raise. In my mind Babcock was a stable, boring business with fairly predictable revenues, being priced like a cyclical due to the negative effects of social distancing on its contract profitability.

After a nervous wait and much Twitter abuse/pity due to my bullish stance, the new CEO David Lockwood announced the sale of non-core assets and his plan to right the company without raising additional capital. The stock rose over 30% that day, proving once again that good things can happen on ordinary news to the deepest of value stocks.

Summary

It has been another bizarre six months in global markets. Certainly very few predicted that we would still be battling lockdowns and new strains 18 months after the onset of the Covid pandemic or that the US Capitol would be stormed by election protestors, but despite this, undervalued stocks had a great six months.

While the gloabl indexes remain close to the most expensive they have ever been, it remains possible to put together a portfolio of remarkably cheap holdings and this is what I have been and will continue to work at.

Thanks again to everyone who gave feedback and discussed ideas over the first half, I appreciate your aid and support. Please fire away with any feedback or queries.

I hold postions in Gazprom, Cameco, Micro Focus, Petrobras, Babcock International, ABS CBN, Barrick Gold, Saipem, Antero Resources, Telefonica Brasil, Aimia and Lilak.

Guy

As always (and especially when I'm mentioning so many stocks), this isn't investment advice. Please do your own due diligence and seek professional advice if you're unsure about your finances.