Following Up Ping An

Following Up Ping An

My recent post on Ping An ended up being easily the most viewed in 18 months of writing this blog. The huge advantage being that I received a lot of quality feedback and have spent much further time mulling the company. So today I will briefly highlight some of what I have learned and outline my current thinking with regard to asset/Evergrande risk, competition and valuation.

Asset/Evergrande risk

Are you even a financial journalist if you haven’t written a recent article likening Evergrande to China’s “Lehman moment”? Despite the sensationalism, people calling catalysts to bring down financial systems have a pretty poor track record. Could there be a bust, with significant contagion? Possibly, but we just don’t know and it is preferable to be having this discussion with Ping An already down 50%, somewhat discounting the risk and already reflecting the market’s fears.

It is certainly true that Ping An’s (and many Chinese financials') assets are something of a black box. In fact, it is reasonable to think there could be substantial bad credit in the Chinese system given this decade’s build-up of banking assets in the Middle Kingdom. However, this is now very much a “known” risk and anything less than catastrophe could be wildly bullish for the stock price.

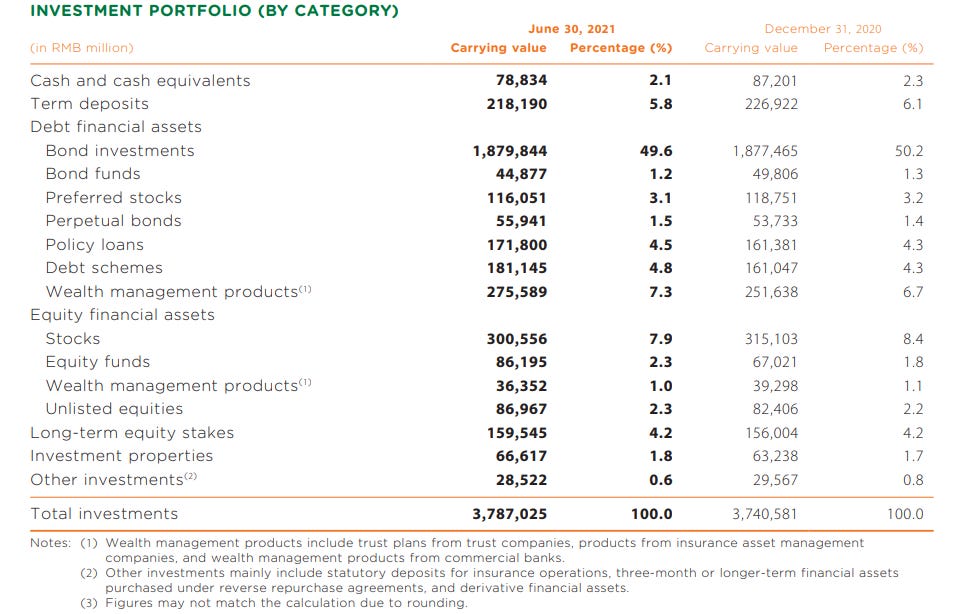

In my original article, I broke down Ping An’s property exposure and imagined a scenario where half of it is written off, but in a “Lehman” scenario, this would certainly not be punitive enough. Consider that the company’s invested float (see below) contains 1.9tr RMB of bond investments, as well as potentially troublesome exposure to Wealth Management Products (WMPs) and other property developers, compared to 1tr RMB in consolidated group equity. The worst-case scenario would be severe, such is the nature of leveraged financial institutions.

Asset quality is also very important to Ping An when assessing its Embedded Value (EV). As previously discussed, the company is currently priced as if it will not only never write profitable insurance again, but that it will lose money on many existing policies. Of course, this is dependent on the reliability of this underlying EV.

Ping An currently uses an assumption that it will achieve a 5% annual return on its float in making this calculation, which is not a given when you are forced to hold as much fixed income as a major insurer. The company’s return on this measure last year was 5.3% and it isn’t hard to imagine a rough period undermining this value in a downturn. It is also a valid fear that a low return environment would tempt institutions with return mandates to reach out the risk curve and end up in more debacles, such as China Fortune Land.

Competition and EV

I was quick to blame Covid for Ping An’s slump in fundamental growth last year. While this certainly played a part, competition is also eyeing off the huge potential in Chinese life insurance.

This can be seen most prominently in the sharp declines in operating return on EV and falling New Business Value (NBV), presented here with 2020 on the left and descending to the right.

Source- Company filings

While this is a concern, the company has all the advantages of market leadership and is wielding them as best they can. I discussed their efforts to digitalise their business, in particular their Life customer recruitment and management, in my previous post and struggle to see other firms competing with this technology and scale. Despite a tougher landscape, I believe the sheer growth ahead of Chinese life insurance means there will be more than enough room for the continued dominance of Ping An.

Adjustment for this could be made by lowering EPS growth assumptions, such as the 15% I used previously (being significantly below the five-year average) or an even more conservative number, as the business is currently priced to stagnate, at around 6x earnings.

Valuation

On balance, I still believe Ping An is too cheap and has an exceptional, probabilistic-weighted return. However, given the wide dispersion of macro risks and opacity of the Chinese financial system, it is also unsuitable as a concentrated position and should be sized according to large impairment being one possible outcome.

In my previous post I used a target multiple of 15x and I am sticking with it. I have had great feedback suggesting a current fair value of 10x, but when I analyse a company, I am attempting to look through the cycle to when EM sentiment has improved and Ping An is “investable” again, even if this is several years away. I see this as a reasonable target in a favourable market, as opposed to a strict and conservative fair value.

After all, Ping An traded at 11x as recently as December 2020, and 15x would imply around 2.5x book, which I view as more than possible for a growing equity base, achieving a high-teens operating ROE (2020- 19.5%).

Thanks for reading.

Guy

As always, this isn’t investment advice. Please do your own due diligence and seek professional advice if you’re unsure about your finances.