Daring to Be Great

Daring to Be Great

Howard Marks is justifiably revered in value investing circles for an ability to decipher finance in a simple way, possibly second only to Warren Buffett himself. My favourite memos of his relate to the 2006-10 period, as he chronicled the GFC with great prescience, and none more so than his 2006 piece "Dare to Be Great".

Named for a 1970's conman, Glenn Turner, who would arrive to a new town under a banner reading "Dare to Be Great", before shilling tapes purported to contain the secret to getting rich, the memo is a thoughtful discussion of what it actually takes to outperform the crowd.

I won't dwell on the memo too much, as you can read it for yourself and I'm unlikely to do it justice, but it speaks to the deep contrarian streak that has made Marks so successful. The question is rightly posed- how can you do better than the crowd if your portfolio looks exactly like everyone else's?

Marks is rightly highly respected today, but the reality is that in real time, many of his most successful investments would have had his clients (and possibly Marks himself) holding their noses and even questioning his judgement. Those portfolios looked drastically different to Wall St consensus at the time and get to the crux of the article- you can achieve comfort within the crowd and live or die with the masses (average/mediocrity) or you can stand apart and position yourself for large individual success (or catastrophic failure).

Marks sums it up concisely:

Non-consensus ideas have to be lonely. By definition, non-consensus ideas that are popular, widely held or intuitively obvious are an oxymoron. Thus such ideas are uncomfortable; non-conformists don't enjoy the warmth that comes with being at the centre of the herd.

Large allocation firms have long made their preference clear- occupying the crowded average is a very safe way to do business, ensuring a generous flow of fees in good times and the "everyone's down" defence in bad.

If you follow my blog, I'm sure that you have a contrarian leaning, so I will pivot to the question at hand- how does an investor "dare to be great" in today's markets?

With the S&P 500 CAPE (10yr Cyclically Adjusted PE) blasting through 35x, I would argue strongly that it is not in US large caps. Some have dubiously argued that because the ratio went as high as 40x in 2000, there is room to run. I won't rule it out, but believe that any gains from here will be swiftly given back when the cycle turns. Needing a run to the highest previous levels in history to justify your investments is not a viable strategy.

That mature US defensives, such as Coca Cola, McDonalds and J&J, are trading with PEs in the 30s are blatant signs of excess in my opinion, without even having to start on the NASDAQ. Even US value stocks and cyclicals have had a great run recently and now sit above their historic norms- not expensive, but not a bargain either. It is the record spread between growth and value that has them looking relatively spectacular.

This is why I currently have only one 2% position in the US. It seems plain that this is where the cheery consensus can be found today. So where's the pain?

I wrote in my 2020 performance review about the Emerging Markets, the UK and energy being the three pillars of my portfolio and given that I am aiming for extremely low turnover, and valuations haven't changed much, that remains the case today.

Emerging Markets

The current CAPE in the Emerging Markets remains 60% below the US at 15x. The chart below shows the consistent pummelling EM equities and currencies have taken relative to developed markets over the last seven years, with only a modest relative uptick coming since the US election and vaccine news giving some light at the end of the tunnel.

The news gets even better for those willing to consider the Emerging Markets, with the tragic relative performance of value to growth. As in all parts of the world, value remains historically cheap in comparison to growth in EM, the difference being that it not just relatively but also absolutely cheap with a CAPE of 11x.

A stockpicker's advantage is, of course, the ability to selectively add the cheapest of the cheap within the asset class and I have added to holdings in Brazil, Russia, South Korea and developing Asia at generous free cash flow yields and NAV discounts, over the last year.

The UK

Similarly, valuations in the UK have been battered over the last five years, with rolling bad sentiment from Brexit, political instability and now Covid, seemingly an unending wave of bad news. However, as I have written before, all of these factors are close to being resolved one way or another and the this will lift the veil of uncertainty engulfing UK markets.

Rob Arnott's Research Affiliates agrees and recently called UK value stocks as their "Trade of the Decade" in their excellent paper "How COVID-19 Vaccines and Brexit Create the Trade of the 2020s", stating UK equities are:

"trading in the cheapest quintile of their historical norms based on both price-to-book and price-to-five-year average cash-flow ratios, and in the bottom third, based on price-to-five-year average sales ratio."

The following chart shows RAFI's expected returns, with the UK their favoured market.

For believers in mean reversion, it is not necessary to know the exact path or catalyst to outperformance, but enough to remember the multitude of historical instances the UK has traded at a premium to the US and enjoy the generous dividend yields on offer while waiting.

It seems clear to me that, for better or worse, Brexit and Covid will be considered distant events by 2030 and the time to have taken positions will have been while the fear was still strong. This why I currently have three UK value holdings making up 30% of my portfolio and, in my opinion, the gains they have enjoyed since the vaccine news are only the beginning.

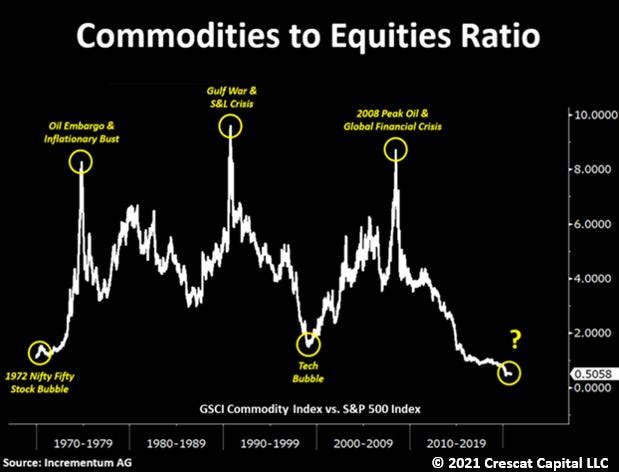

Commodities

The third pillar remains energy and commodities, which are still extremely cheap, despite performing strongly since I wrote about them here. Crescat's excellent chart sums up the historic magnitude of the set-up, below.

Sceptics have written off traditional commodities as victims of the ESG movement. I agree that the world needs to transition to a lower carbon future, but how do we handle the interim? Rather than preventing necessary energy sources access to capital, I would advocate for the lowest carbon-intensive, viable energy sources we currently have (uranium and natural gas) to play a large role as transition fuels while we are building out to renewables.

The Energy Information Administration(EIA)'s 2050 projections estimate that, while renewables will rise sharply (supplying nearly 30% of global power by 2050), depressingly, coal will still be supplying a significant percentage of global power, largely due to sharply higher global energy demand from the burgeoning global middle class. It also indicates that tales of oil's demise are greatly exaggerated.

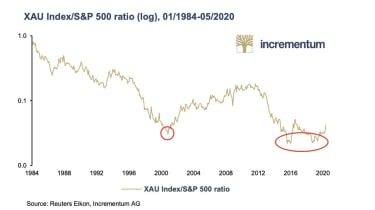

The situation is similar in precious metals, with the XAU Gold and Silver Miners index only just rising off its lows against the S&P 500 (shown below). A strong argument can also be made for owning gold to protect against inflation, with recent research, by both Schroders and Verdad Advisors, indicating that gold and commodities are the best performing assets in inflationary environments.

Japan

Excitingly, GMO recently published an insightful piece on a potential new corner of opportunity to which I have no exposure, as yet. The piece, "Japan Value: An Island of Potential in a Sea of Expensive Assets", highlights the left-for-dead valuations in Japanese small caps, pointing out their 4th percentile cheapness and current 45% discount to the Japanese TOPIX index (the average being 25%). The market long having been a curiosity to value investors, with its almost non-existent bankruptcy rates and cash-rich balance sheets.

Daring to Be Great in 2021

So how do opportunities like these exist in a world of nose-bleed valuations? Negative momentum and, what Lyall Taylor has referred to as, liquidity flywheels. As large-cap tech stocks have roared higher, investors have sold non-US value stocks to get in on the momentum party, creating a virtuous cycle.

It takes courage to buy something that has been going down for a long time. Value investors have been early to these sectors over the last several years, but the future returns on offer have grown with the subsequent falls. There is the fear of being caught in a value trap, but intrepid investors must remember that, without this perception, the valuations wouldn't exist.

In my opinion, it is these beaten down sectors that give investors the chance to "dare to be great" today. Investing over a full-cycle timeframe and ignoring the day-to-day noise is easier said than done, but a portfolio of durable EM, UK, commodities and possibly Japanese value stocks gives the best chance of standing apart from the crowd and reaping the potential benefits.

This is the sort of measured contrarianism I believe Marks had in mind when penning his timeless memo.

Guy

As always, this isn’t investment advice. Please do your own due diligence and seek professional advice if you’re unsure about your finances.